If You Can Afford the 30-Year Mortgage Now, Why You Should Choose the 50-Year Mortgage

real estate Darren Koenenn November 10, 2025

real estate Darren Koenenn November 10, 2025

Choosing a 50-year mortgage over a 30-year isn’t about affordability; it’s about financial optimization. If you can afford the 30-year payment today, opting for the 50-year version can free up cash flow to invest the difference. If those invested savings compound faster than the extra interest you’d pay, you can come out dramatically ahead owning the same house outright sooner, with extra capital left over.

Loan amount: $400,000

Interest rate: 5.00% fixed

30-year monthly payment: $2,147.29

50-year monthly payment: $1,816.56

Monthly savings (to invest): $330.73

Investment vehicle: S&P 500 index (10.5% nominal long-run average return)

| Term | Total Interest Paid | Total Payments | Difference |

|---|---|---|---|

| 30 years | $373,023 | $773,023 | — |

| 50 years | $689,933 | $1,089,933 | +$316,910 |

You save $330/month but pay about $317k more interest if you keep the 50-year loan to maturity.

That’s the cost of leverage and flexibility. The question is: can your invested difference beat it?

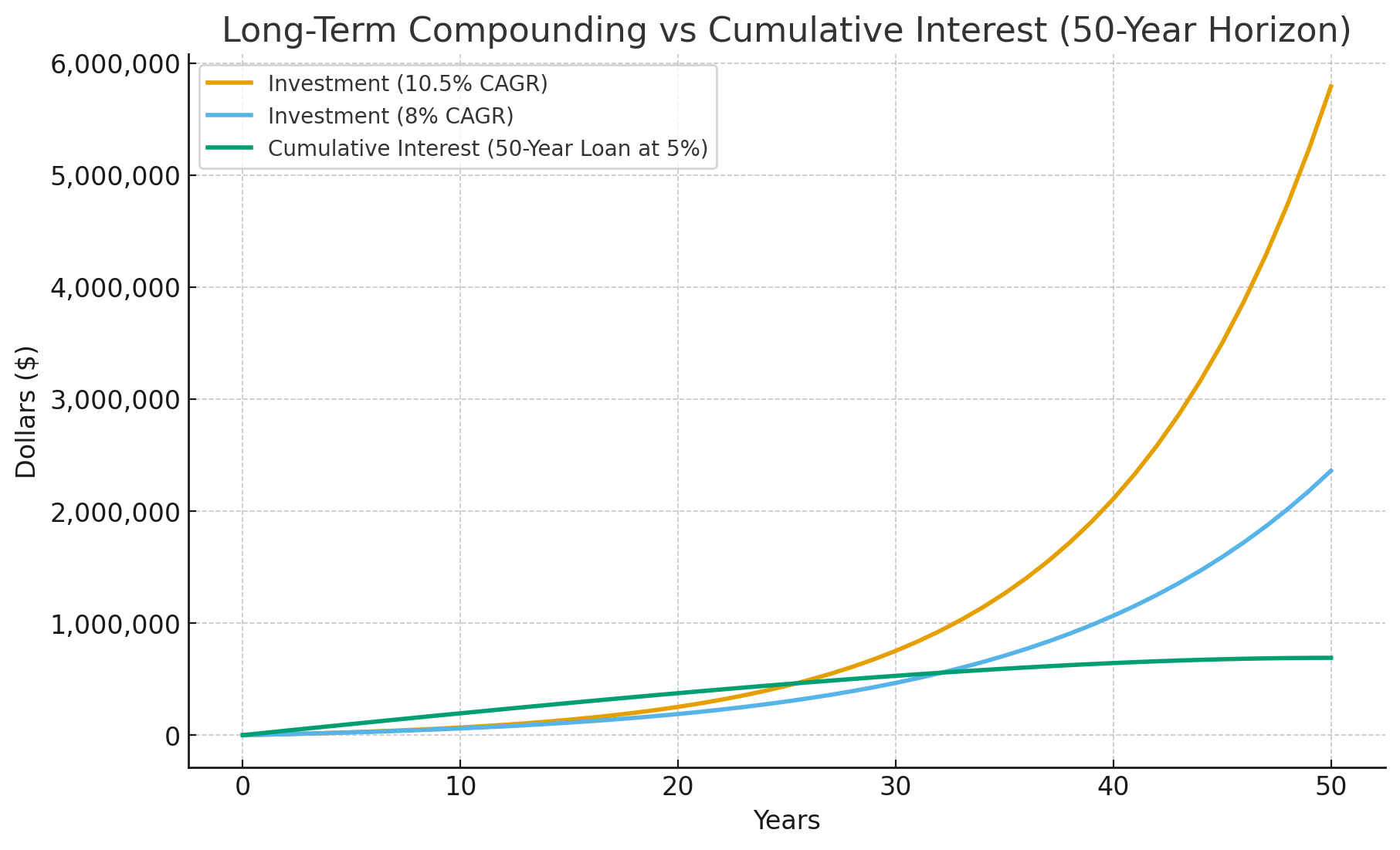

If you invest that $330.73/month at the S&P 500’s long-run average of 10.5%, your portfolio could grow as follows:

| Year | Portfolio Value |

|---|---|

| 5 | $25,628 |

| 10 | $67,850 |

| 15 | $137,408 |

| 20 | $252,001 |

| 25 | $440,786 |

| 30 | $751,800 |

At 30 years, your invested savings would total $751,800, easily surpassing the mortgage’s extra interest.

But that’s the pre-tax scenario; let’s be realistic and apply taxes.

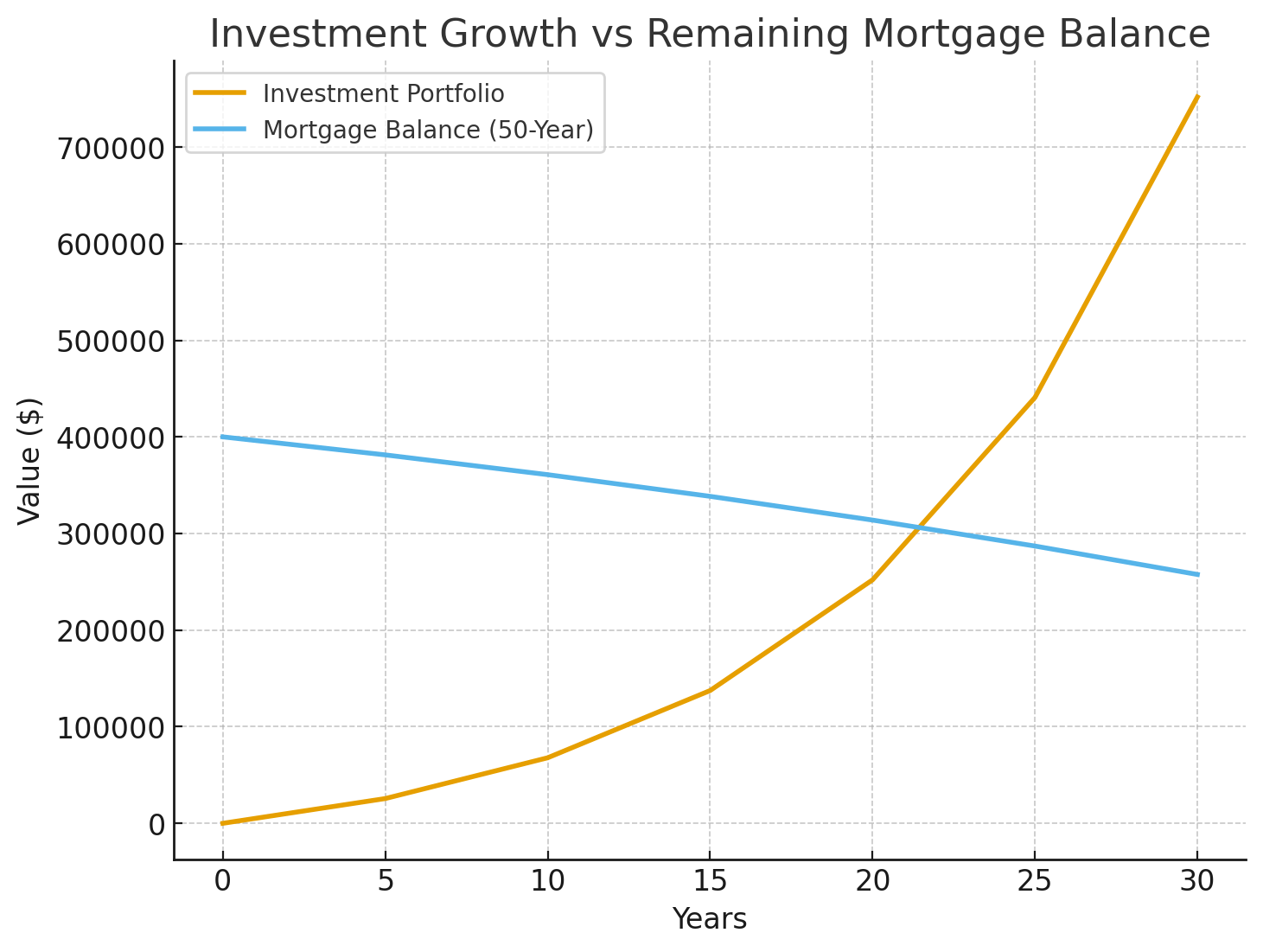

Assuming a 15% long-term capital gains rate, 2% dividend yield, and reinvestment of after-tax dividends, your portfolio could still grow fast enough to pay off the entire 50-year mortgage around Year 25.

| Year | After-Tax Portfolio | Mortgage Balance | Payoff Possible? |

|---|---|---|---|

| 20 | $252,000 | $313,878 | ❌ |

| 25 | $440,786 | $286,992 | ✅ Yes — crossover around Year 25 |

| 30 | $751,800 | $257,582 | ✅ |

Even after taxes, the investment strategy allows you to pay off a 50-year mortgage five years sooner than the standard 30-year payoff, while maintaining flexibility and liquidity.

If instead of stopping once you could pay off the house (around Year 25), you continued investing that $330.73/month for the full 50 years, your portfolio would grow to approximately $5.79 million.

That’s a $5.8M portfolio built simply by redirecting the payment difference into the market rather than the bank.

Even under a more conservative 8% return, that same strategy would still result in around $2.36 million over 50 years.

This long-term compounding shows the real power of opportunity cost—paying off your mortgage early means losing decades of exponential investment growth. For disciplined investors, this approach shifts the question from “When can I pay off my home?” to “How large can I grow my wealth while owning it?”

The two lines cross at Year 25, showing the moment your invested savings could fully pay off the mortgage.

If you direct those monthly savings into a Roth IRA, the dynamic improves even further:

All growth is tax-free (no capital gains or dividend taxes).

The crossover moves up to around Year 24.

Every dollar earned beyond that point is pure, tax-free compounding.

For disciplined, high-income earners who qualify (or can use a backdoor Roth), this structure makes the 50-year strategy especially powerful.

Mathematically: The 50-year mortgage can outperform the 30-year if the savings are invested consistently in growth assets.

After-tax, real-world: You could pay off your home in about 25 years with the investment proceeds five years sooner than a 30-year loan while maintaining liquidity and flexibility.

With a Roth IRA: You unlock tax-free compounding, accelerating your payoff and maximizing long-term net worth.

If you have the discipline and long-term mindset, the 50-year mortgage isn’t about stretching affordability; it’s about engineering financial efficiency.

A 50-year mortgage can be a smart choice for financially disciplined borrowers who use the lower payment to invest the difference. If your investments grow faster than the additional interest costs of the longer loan, you could come out ahead—owning your home sooner while building extra wealth.

The main reason is cash flow optimization. A 50-year mortgage reduces your monthly payment, freeing up hundreds of dollars that can be invested elsewhere. Over time, those invested funds can grow exponentially, potentially offsetting the higher interest cost and generating long-term financial gains.

The key risk is investment discipline. If you don’t actually invest the monthly savings or if your investments underperform you’ll simply end up paying much more interest over the life of the loan. The strategy only works if you consistently invest the difference and stay the course through market ups and downs.

In the example provided, investing at the S&P 500’s long-term average return of about 10.5% easily beats the mortgage’s 5% rate. Even after taxes, the “crossover point” (when investments can pay off the mortgage) happens around Year 25. With more conservative returns, say 7–8%, you still build significant wealth over time, though the crossover may take a bit longer.

Yes! Using a Roth IRA can supercharge this approach. Because all growth is tax-free, your investment crossover point may arrive around Year 24 instead of 25, and every dollar earned beyond that compounds tax-free for the rest of your life. It’s an especially effective setup for high-income earners with long investment horizons.

Interest rates and market returns will always fluctuate, but the core principle remains: investing the payment difference creates optionality. If returns are lower, your advantage narrows; if higher, your wealth grows faster. The flexibility of having liquid investments versus home equity also gives you more control over your finances.

No. A 50-year mortgage isn’t ideal if you’re close to retirement, expect to move soon, or prefer being debt-free. It’s best suited for long-term investors who have stable income, solid credit, and the discipline to consistently invest their savings rather than spend them.

If you invested the difference ($330.73/month) for 50 years at the S&P 500’s historical 10.5% return, your portfolio could grow to around $5.79 million. Even with a conservative 8% return, you’d still amass roughly $2.36 million, a powerful testament to long-term compounding.

Absolutely. Most lenders allow early repayment without penalties. You can always pay extra or use your investment gains to pay off the balance early giving you flexibility that a shorter loan term doesn’t offer.

The 50-year mortgage isn’t about stretching affordability, it’s about engineering financial efficiency. When paired with disciplined investing, it can outperform a traditional 30-year mortgage, helping you own your home faster and grow your wealth more substantially in the long run.

Stay up to date on the latest real estate trends.

30a

We pride ourselves in providing personalized solutions that bring our clients closer to their dream properties and enhance their long-term wealth. Contact us today to discuss all your real estate needs!

KOENENN GROUP

2048 W COUNTY HIGHWAY 30A STE 107 SANTA ROSA BEACH FL 32459